Exploring the Connection Between Student Loan Debt and Reduced Fertility Rates in the United States

Source: Unsplash

Introduction

Recently, the trend of globally declining fertility rates has been making headlines. In the United States, the downward trend in fertility rates is a contentiously debated issue and far-right political narratives have captured the discussion, framing low fertility rates as a looming crisis that will lead to the end of humanity (Sherman 2025; Politico 2024). This is an extreme and alarming claim warranting the necessity to investigate the reasons for declining fertility rates and potential policy responses outside the dominant framing of far-right politics.Common arguments credit changing generational priorities and values, increased female labor force participation, and declining marriage rates as causes of declining fertility rates. However, this article argues that student loan debt could be an important overlooked financial constraint shaping young adults’ decisions about marriage, homeownership, and family formation.

Demographic Context

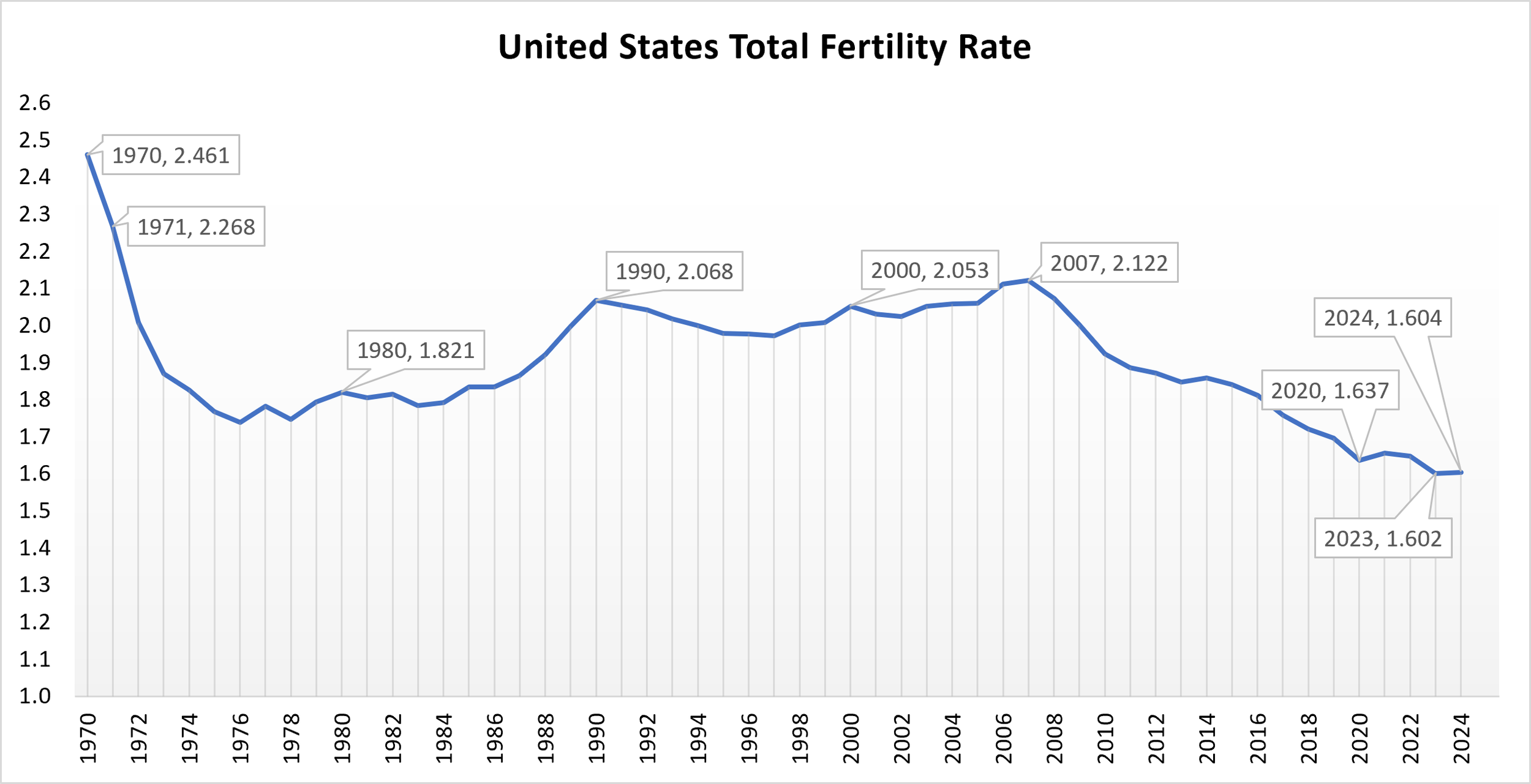

Source: Graph created by author using data from the Human Fertility Database

Since the 1970s, in many high-income countries including the United States, fertility rates have declined due to the introduction of and access to contraception, the right to abortion, easier access to higher education, and increased labor market participation, as well as delays in the age of marriage and decreasing child mortality rates (Goldin and Katz 2022).

As women delayed marriage and starting a family to pursue higher education and a career, the age at which Americans had their first child increased. As women tend to have fewer children as they age with the biological childbearing window shrinking, the delay in childbearing contributes to a lower total fertility rate. Hence, total fertility rates trend steadily downwards from the 1970s before plateauing in the 1990s and early 2000s. However, beginning in 2007, the United States experienced a renewed acceleration in fertility decline. The total fertility rate fell from 2.12 in 2007 to a historic low of 1.60 in 2023. This post-2007 shift has puzzled researchers and policymakers because it suggests that more recent economic and social changes may be reshaping family formation departing from previous explanations.

Potential Causes of the Accelerating of Declining Fertility Rates

Researchers have proposed several explanations for the post-2007 fertility decline, including changing gender norms, shifting generational priorities, the effects of the Great Recession, and rising economic inequality (Bloom et al. 2025; Adashi et al. 2026; Goldin 2025; Doepke et al. 2022). The Great Recession likely played an important role as many Americans faced stagnant real wages, job insecurity, housing loss, restricted access to credit, and reduced financial resources. Under these conditions, many Americans possibly delayed having children until economic prospects improved. However, Kearney et al. (2022) find that fertility declines after the Great Recession were consistent across age groups and cannot be explained by cyclical economic factors alone. This raises an important question: are deeper structural economic conditions now playing a greater role in determining whether young adults feel able to start a family?

Historically, income and fertility were negatively related meaning that lower-income individuals tended to have more children, while higher-income individuals tended to have fewer. In the 21st century, however, this relationship appears to have weakened or even reversed in some countries. For example, Van Wijk (2024) finds that income became increasingly positively associated with fertility in the Netherlands from 2008 to 2022. While this evidence cannot be directly applied to the United States, it suggests a broader shift in that financial security may now be increasingly important for family formation, especially among low- and middle-income individuals (Doepke et al. 2024).

In this context, the post-2007 decline in U.S. fertility may reflect not only cultural change but also the growing difficulty of reaching the economic milestones that often precede parenthood.

The Argument for the Role of Student Debt

One financial constraint facing many young Americans is the rising burden of student loan debt. Since the mid-1990s, the cost of higher education has approximately doubled after adjusting for inflation. As tuition increased, more students relied on loans to finance college, particularly among the middle class. Many young adults now graduate with substantial student loan debt when they are entering the labor market, forming relationships, searching for housing, and making decisions about whether and when to have children.

This overlap motivates a key question: to what extent is the rise in student loan debt associated with declining fertility rates in the United States?

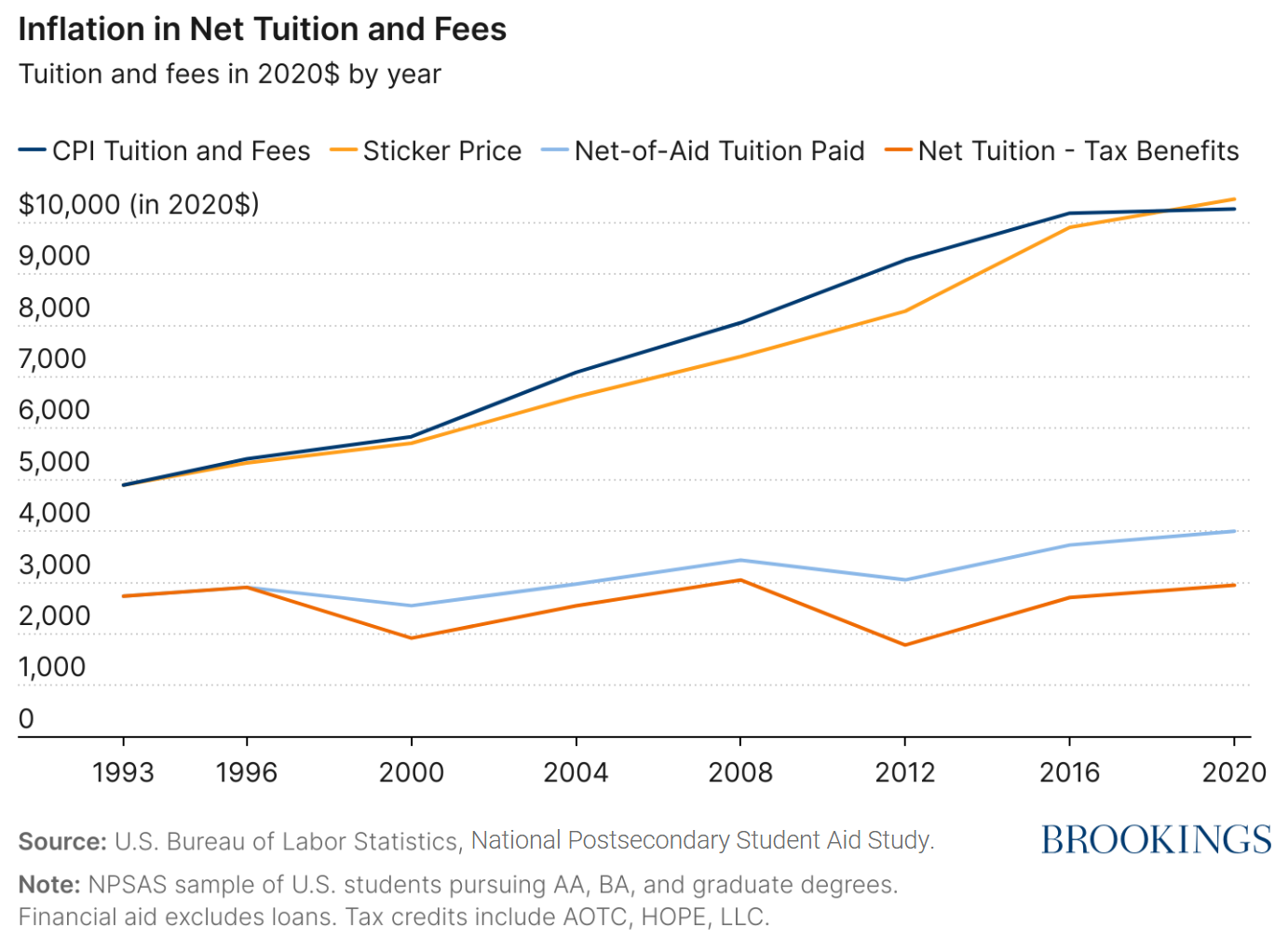

Source: Looney 2024

To finance higher education, students increasingly rely on federal, state, and private loans. Since 2010, student loan debt has become more common among college-educated young adults in the United States. By 2025, total student loan debt held by Americans had tripled since 2007, reaching $1.6 trillion (Nadworny 2025). In the same year, the average student loan debt at graduation was nearly $40,000 (Hanson 2026). The United States is a particularly important case because of the high cost of higher education and the high rate of college attendance. Between 2012 and 2022, 40% of 18- to 24-year-olds were enrolled in college (National Center for Education Statistics 2024). If a large share of young adults attend college and many rely on loans to do so, student debt becomes not merely an individual burden but a common financial condition shaping early adulthood.

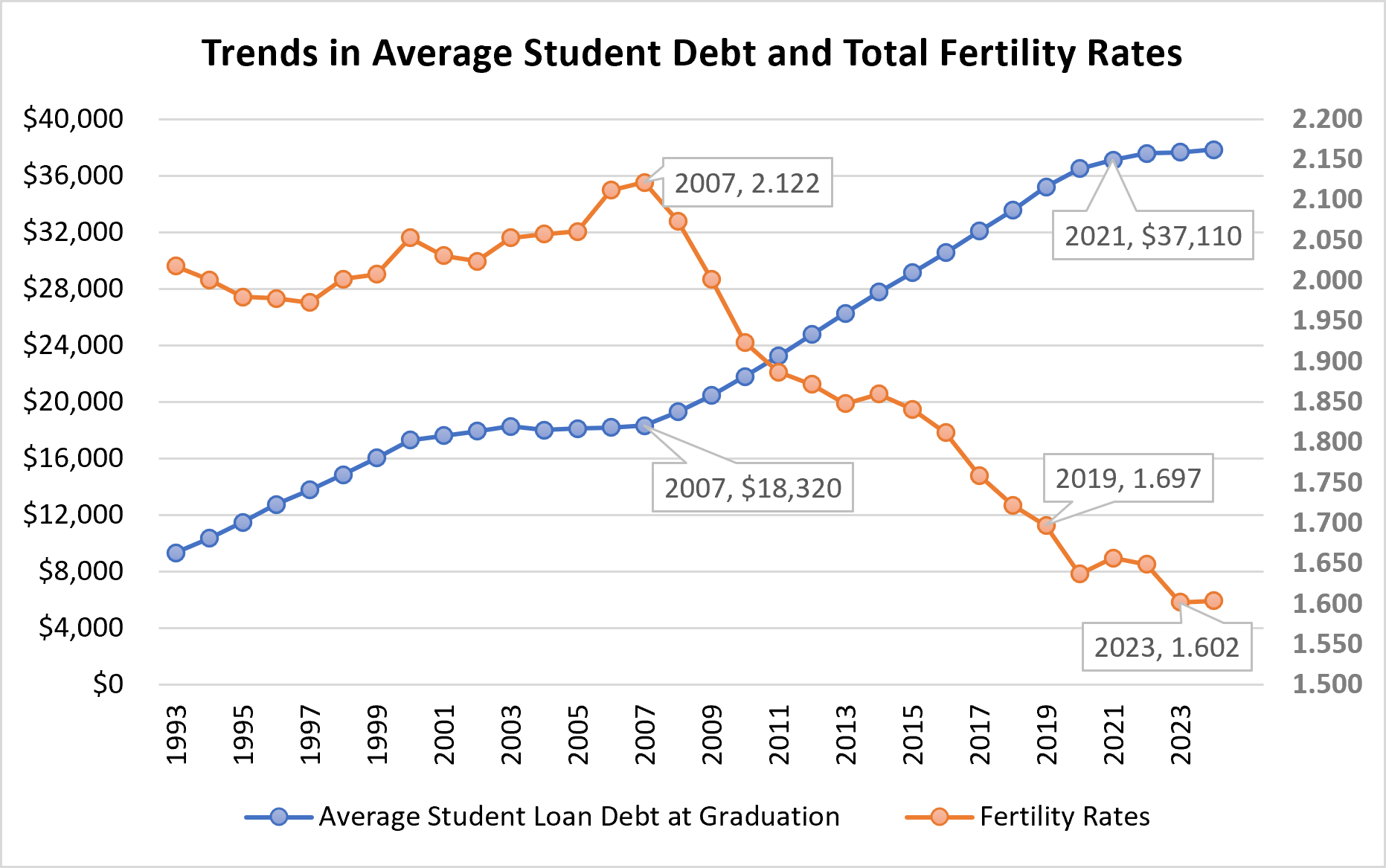

Source: Graph created by the author based on data from the Human Fertility Database and the US Department of Education (Hanson 2026)

The rapid rise in student debt coincides with the accelerated decline in fertility. This correlation does not prove any meaningful causation in the decline of fertility rates, but the simultaneous timing of these trends suggests that student loan debt may be one of several financial pressures affecting young adults’ long-term decisions. Student loan debt differs from mortgage debt and credit card debt because it is a long-term unsecured liability while mortgages are tied to an asset (e.g., a place to live) and credit card debt is typically shorter-term. Student loan debt, by contrast, is often repaid in monthly installments over 10 to 20 years and can carry substantial interest rates depending on the type of loan (Hanson 2025).

A growing body of literature examines this correlation analysing the effects of student loan debt on young adults’ life choices. Addo et al. (2019) find that student loan debt increases the likelihood of cohabitation as young adults seek to reduce living costs, while also delaying marriage. Monthly student loan debt repayments can also hinder wealth accumulation. This matters because wealth, not only income, is often important for family formation. Schneider (2011) shows that wealth is an important prerequisite for marriage. Nitsche and Hayford (2020) show that postponing marriage, particularly among the college-educated, is associated with lower rates of parenthood. Since marriage often remains an important milestone before starting a family, student debt may indirectly delay fertility by delaying marriage. If student loan payments reduce young adults’ ability to save, purchase a home, or build financial stability, they may also reduce the likelihood that individuals start a family.

The most direct evidence linking student loan debt to fertility comes from Nau et al. (2015). Using data from the National Longitudinal Survey of Youth, they find that student debt has a nonlinear negative effect on the transition to first birth from 1997 to 2009. A $1,000 increase in student loan debt is associated with a 1.2% decrease in the annual probability of transitioning to parenthood for women, though the effect is not statistically significant for men. The effect is especially pronounced at higher debt levels. Nau et al. (2015) also find that mortgage and credit card debt are positively associated with, or precede, parenthood. This supports the argument that student debt is distinct from other forms of debt. Mortgage debt may signal stability and asset-building, while student debt may represent a long-term financial burden without any immediate or anticipated return.

Taken together, the literature suggests that student loan debt may depress fertility by reducing disposable income, delaying marriage, weakening wealth accumulation, and making young adults less financially secure during the years when many would otherwise consider starting a family. Student debt may therefore be a substantially overlooked factor shaping fertility decline in the United States.

Limitations of this Argument

There are several limitations to this argument that should be considered. First, measuring fertility decisions requires long and detailed data. A longer panel spanning the full reproductive years of both women and men is needed to determine whether student debt delays childbirth temporarily or permanently reduces completed family size. If individuals with student debt eventually have the same number of children later in life, then student debt may primarily affect timing. If they do not, then student debt may contribute to a long-term reduction in fertility. This means that the effect of student loan debt on family formation cannot be determined until women have completed their childbearing years. Hence, it makes it difficult to understand the long-term effect and development appropriate policy responses.

Second, the COVID-19 pandemic complicates the interpretation of recent fertility patterns. Fertility rates increased slightly during the pandemic (Bailey, Currie, and Schwandt 2022), but it is difficult to determine whether this was due to lockdowns, social distancing, changes in work arrangements, or the pause on federal student loan repayments. From 2020 to 2023, individuals holding federal student loans were not required to make monthly repayments. This unusual policy period may offer suggestive evidence, but it also makes causal interpretation more difficult.

Third, existing studies often do not account for time since graduation. This is an important gap because the impact of student debt may vary depending on how long an individual has held the debt and where they are in their career trajectory. A person who has just graduated may experience student debt very differently from someone who has held debt for ten years.

Finally, most studies do not distinguish between debt incurred for undergraduate and graduate education. This distinction matters because individuals who take on debt for graduate or professional degrees may differ systematically from those who take on debt for undergraduate study. For example, those pursuing specialized graduate degrees may be more career-oriented or may expect higher future earnings. In such cases, delayed family formation may reflect professional ambition, financial constraint, or both.

These limitations mean that student debt should not be treated as a single-cause explanation for declining fertility. However, they do not undermine the broader argument that debt deserves more attention in debates about family formation and demographic change.

Conclusion

As student loan debt becomes a greater financial burden for young Americans, it may increasingly shape whether and when they feel able to start a family. Fertility decline is often discussed through the language of culture, values, female autonomy, or individual preference. Yet these explanations are incomplete if they ignore the economic conditions under which young adults make decisions about partnership, housing, marriage, and parenthood.

Student debt does not force people to have fewer children in a simple or deterministic way. Rather, it changes the conditions under which family decisions are made. Monthly loan repayments reduce disposable income, delay wealth accumulation, and make long-term planning more uncertain. For many young adults, especially those without family wealth, student debt may turn parenthood from a desired life step into a financial risk.

This matters because policymakers should move beyond moralizing narratives and focus on reducing the economic insecurity that makes family formation difficult. Policies that lower the cost of higher education, reduce the long-term burden of student loans, support affordable housing, and expand access to childcare would do more to address fertility decline than alarmist rhetoric about demographic crisis.

Ultimately, the goal should not be to pressure individuals into having children. It should be to create conditions in which people who want children are not prevented from having them by debt, insecurity, or the rising cost of adulthood. Therefore, student loan debt is not only an education policy issue, but also a family policy issue, a housing issue, and a broader question of economic security for younger generations.